Short Selling vs. Buying Puts: Which Strategy Fits You?

Betting on a drop can feel smart, but which tool should you use? Short selling vs. buying puts looks similar on the surface, yet the risk, cash outlay, and rules are very different. Here is the plain version: short selling means you borrow shares and sell them, hoping to buy back lower; a put option gives you the right to sell at a set price, and your max loss is the premium you pay.

This guide shows you the real trade-offs, the hidden costs, and how to pick a bearish approach that matches your risk, your account size, and your pace. Rules and fees in 2025 still matter, and both methods can lose money fast. Use the quick pick guide later in the post to match your style. This is education, not advice.

Short Selling vs. Buying Puts: The Simple Difference and When Each Shines

Both strategies aim to profit when prices fall, yet they work differently.

Short selling is a trade you enter by selling shares you do not own. You borrow the shares through your broker, sell them first, then try to buy them back cheaper. It often has a lower upfront cost, but risk is open-ended if the stock rises. It can also come with borrow fees and availability constraints that change daily.

Buying a put is different. You pay a premium for the right to sell shares at a set strike price by a set date. Your risk is defined, capped at the premium, and you do not need to borrow shares. The trade-off is time decay. If the stock does not drop enough, fast enough, the option can lose value even if you are directionally right.

Core trade-off: shorting can be cheaper at entry and has no time decay, but it carries unlimited loss and borrow friction. Puts cost a premium and decay over time, yet they cap losses and simplify risk.

Quick rule: if you want capped risk, choose puts. If you want no time decay and easy exits, shorting can fit when borrow is cheap and shares are available.

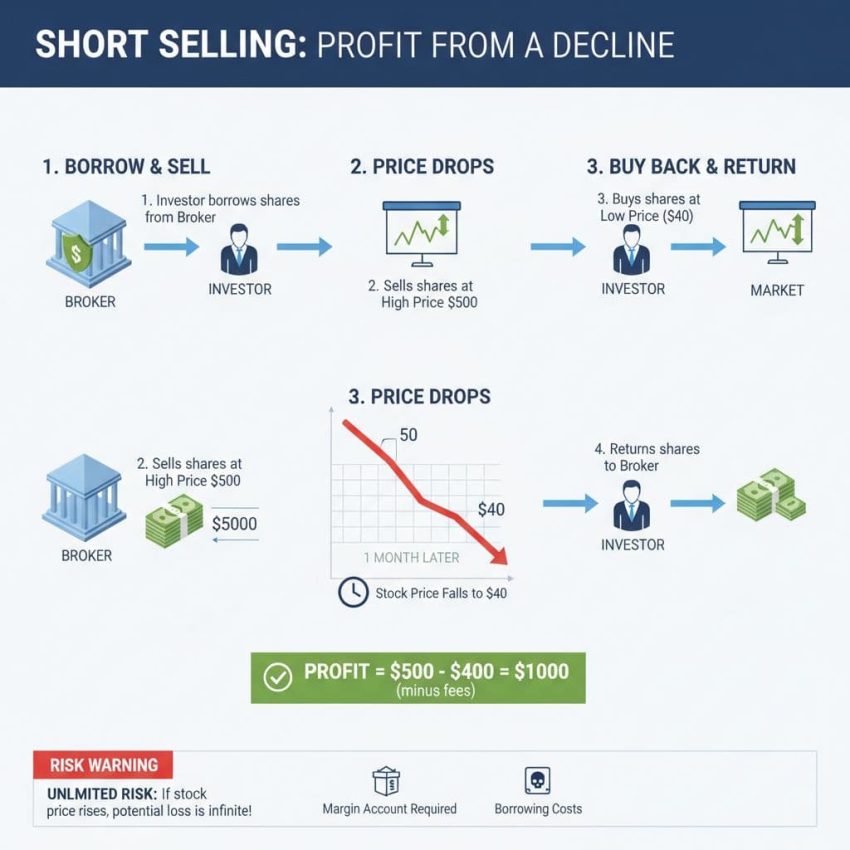

Short selling explained in plain words

- Your broker locates shares to borrow.

- You sell those borrowed shares at the current price.

- You later buy the shares back and return them.

If the price falls, you keep the difference. If the price rises, you owe the difference and your loss can grow as the stock climbs. You need a margin account. You may pay borrow fees, and you could owe cash dividends while short. For a deeper primer, see Short Selling: How It Works.

Buying a put option explained in plain words

- A put option is a contract that lets you sell a stock at a strike price.

- You pay a premium to buy that right.

- You can sell the contract later or exercise it, depending on value and timing.

Your max loss is the premium you pay. The stock needs to fall enough, soon enough, to overcome the premium and time decay. Think of it like insurance that pays off if a drop happens within the policy window.

Pros and cons you can feel in real trading

Short selling pros:

- No time decay.

- Simple charts and price action, just like trading stock.

- Tight spreads in very liquid names.

Short selling cons:

- Unlimited loss if the stock rips higher.

- Borrow fees and interest can add up.

- Margin calls and forced buy-ins during squeezes.

- Shares can be hard to borrow when you want them most.

Buying puts pros:

- Defined risk, capped at the premium.

- No need to borrow shares or worry about recalls.

- Strong payoff on sharp, fast drops.

- Useful for hedging long positions.

Buying puts cons:

- Time decay reduces value day by day.

- Wider bid ask spreads on many chains.

- Implied volatility crush after events can hit hard.

For a clear overview of short selling risks and rewards, read Short Selling: The Risks and Rewards.

A quick pick guide: when to short, when to buy puts

Choose short selling when:

- Shares are easy to borrow and the borrow rate is low.

- The stock is very liquid with tight spreads.

- You expect a steady downtrend, not just a quick dip.

- You can monitor positions often and honor stops.

Choose buying puts when:

- You want capped risk and simple sizing.

- You see a potential sharp drop or catalyst.

- Events like earnings create jump risk.

- Your account is small and you need fixed risk.

How the Money Works: Costs, Risks, and Payoffs

Shorts and puts reward downside moves, but the money profile is very different. A short has linear profit and loss. Every dollar down is a dollar gained per share, and every dollar up is a dollar lost per share. There is no time decay, yet fees and unlimited risk loom.

A long put has a convex payoff. Losses are limited to the premium, while big, fast moves lower can produce outsized gains. The trade can still lose if the drop is too slow or too small. You are paying for probability and timing, not just direction.

Fees matter. Shorts may carry borrow and interest. Options have spreads, commissions, and time decay. Treat these as part of your edge test, not an afterthought.

Short sale profit and loss, with simple math

Example:

- You short 100 shares at $50.

- Stock drops to $40.

- Profit is $10 per share, or $1,000, before fees.

If borrow and interest add $50 during the hold, your net is $950.

Now the other way:

- Short 100 shares at $50.

- Stock pops to $70.

- Loss is $20 per share, or $2,000, plus fees.

A jump can trigger a margin call. If your equity falls below requirements, your broker can close the trade at a bad price. Buy-ins can also happen if the lender recalls shares, which can force a cover during a squeeze.

Put option profit and loss, with simple math

Example:

- You buy one 50 strike put for $2, 30 days out.

- Your cost is $200.

- Breakeven at expiration is $48.

If the stock is $40 at expiration, the option is worth $10, or $1,000. Profit is $800 after subtracting the $200 premium. If the stock is at $50 or higher at expiration, the put expires worthless, and your loss is $200. Along the way, time decay chips away at value if price is not moving enough.

Hidden costs and frictions that trip traders

For shorts:

- Borrow fees can jump with demand.

- Hard-to-borrow names can block entries.

- You owe any cash dividends declared while short.

- Recalls can close your trade early.

- Slippage can spike during squeezes.

For puts:

- Bid ask spreads increase your cost to get in and out.

- Commissions and fees matter for small accounts.

- Time decay accelerates near expiration.

- Implied volatility often drops after news.

- Exercise and assignment near expiration can affect stock and cash.

If you want a community-friendly walk-through, this thread covers the basics in plain language: Can someone explain shorting a stock?

Taxes in the US: what to expect at a high level

Short sale gains are usually taxed as short term gains. Payments in lieu of dividends on shorts are generally ordinary income. Most equity option trades are short term unless held more than a year, which is uncommon for puts. Wash sale rules can apply on related entries and exits. Always confirm details with a tax professional, since your situation and local rules can differ.

Which Strategy Fits Your Account and Style?

Match the strategy to your capital, time, and stress tolerance. Short selling can suit active traders in liquid names who can manage risk minute to minute. Buying puts often fits smaller accounts or traders who want a clear max loss. Long-term investors who want protection often prefer puts for their simplicity and defined risk.

Keep the choice practical, not ideological. The best tool is the one you can use consistently.

Small account or beginner: keep risk capped

Favor buying puts. Your loss is defined, and you do not need margin or borrow. Pick liquid tickers, strikes near the current price, and expirations 30 to 60 days out. This gives you time for the thesis to play out and softens time decay.

Start small. One contract is plenty. Use a preset max loss, like 50 percent of the premium, and honor it. Keep notes. Review your entries, exits, and timing on a weekly basis.

Active trader who watches screens: speed and borrow matter

Short selling can fit large cap, highly liquid names with tight spreads and stable borrow. Use hard stops and scale sizes that respect gaps. Do not fight squeezes. If borrow is cheap and shares are plentiful, you can hold during quiet periods without decay.

Puts can also work for fast drops, yet wider spreads and time decay can hurt scalps. If you trade puts intraday, focus on chains with heavy volume and penny-wide spreads when possible. Keep your holding times short around catalysts.

For a grounded look at mechanics and pitfalls, review Schwab’s overview of short selling risks and rewards.

Investor hedge: protect a stock or a portfolio

Protective puts on a core holding can cap downside without selling shares. Index puts can hedge a basket or portfolio. Put spreads can lower cost by selling a lower strike against your long put.

Shorting as a hedge can be messy. Borrows change, fees vary, and risk is unlimited. For long-only investors, puts are usually simpler and cleaner for risk control.

Earnings and news trades: mind IV and borrow

Before big events, implied volatility often rises, then falls after the news. Puts keep risk defined for surprises, but IV crush can erase gains if the move is small. With shorts, borrow can spike or be pulled near catalysts, making entries harder. Trade smaller, plan exits, and set alerts for both price and borrow changes.

Risk Control and Setup Tips That Save Real Money

A strong setup and strict risk plan beat a bold opinion. Use simple rules that you can repeat every week. Cut losers fast and let winners work only when the trend confirms.

Plan size and max loss before you enter

Use a simple cap, like risking 1 percent of your account per idea. For shorts, set a stop based on price structure, not hope, and stick to it. For puts, your premium is the maximum loss. Decide on management: will you take profits early if you’re up 50 percent, or hold until a target price? Pre-plan both.

Pick the right strike and expiration for puts

For swing trades, target 30 to 60 days to expiration. Choose strikes with delta near 0.30 to 0.40 for balanced risk and reward. For higher conviction, consider strikes closer to the money with delta near 0.60. Avoid ultra-short expirations unless you can watch the trade. The time decay is brutal.

Find liquidity and fair pricing

Trade liquid names. Check option volume and open interest. Aim for tight bid ask spreads. Avoid thin weekly contracts unless there is clear volume. For shorts, confirm share availability and a low borrow rate before you enter. Place trades during liquid hours, such as the first and last 90 minutes, to reduce slippage.

For a fundamentals-first refresher on mechanics, see Short Selling: How It Works.

Know the broker rules in 2025

Buying puts usually requires options approval level 2 or similar. Short selling requires a margin account and enough equity, and many brokers will not allow shorting in IRAs. Pattern day trader rules can limit frequent in-and-out trading if your account is under the threshold. Fees can include borrow charges, margin interest, and small regulatory fees. Check your broker’s current terms before you trade so you are not surprised.

Conclusion

Short selling fits traders who want no time decay and can manage unlimited risk. Buying puts fits traders who want defined risk, event protection, and simpler sizing. Use this quick checklist: your account size, time you can watch, comfort with drawdowns, borrow availability, and whether you need a hedge. Paper trade both methods to learn the flow before risking real capital. Thanks for reading, and consider testing one clean setup this week to build confidence.